It is often said that within the first seven seconds of meeting, people will form a solid impression of who you are and start to determine traits like trustworthiness. While this is a truly scary statistic and one which everyone who interacts with clients need to be extremely mindful of, it is also worth extrapolating this timeframe out a little and considering how new clients are onboarded and integrated into your business.

This becomes especially important if your practice has a growth focus and you are looking to increase the number of clients you serve. Interestingly, our CATScan* Client Satisfaction Survey data shows that in the average Australian advisory business, 55% of clients are aged over 60 and 48% are already retired or no longer gainfully employed – for many firms, new client acquisition will be high on their priority list as they address the challenges of an aging client demographic.

As we thought this through, we were initially not that concerned – after all, the satisfaction levels of your new clients should be through the roof, right? These clients have just been through your fact-find process and shared with you their dreams and aspirations for themselves and their family. You have then taken all of this intensely personal information and using all your experience, put forward a solution that, all going to plan (excuse the pun!), will deliver the desired outcomes.

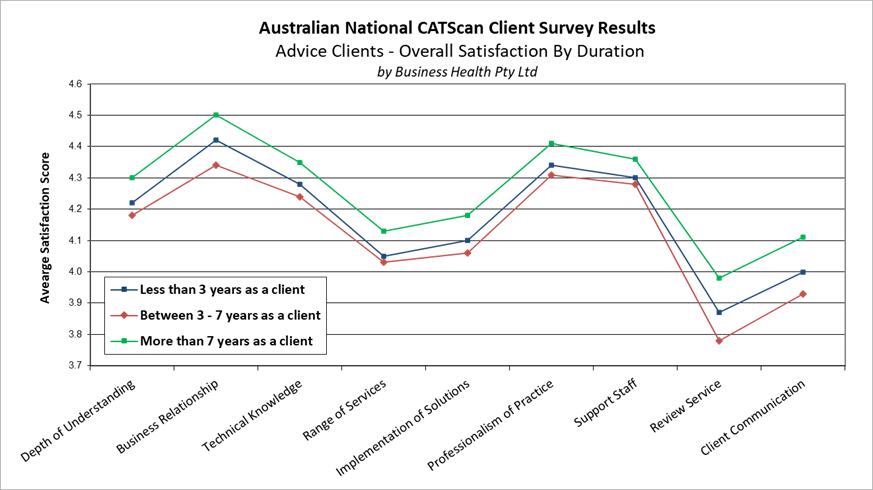

However, as we all know, a cold hard analysis of the facts will always trump assumptions based on intuition or gut feel. Unfortunately, our most recent CATScan analysis provides a healthy dose of sobering realism. The following chart plots the satisfaction levels of new clients versus those that have been working with their adviser for longer periods of time.

It clearly shows that new clients are less satisfied with their adviser’s performance across all nine of the key service delivery areas covered in the CATScan survey (and remember, this is based on over 60,000 “real” clients currently using the services of an Australian adviser).

So, what does this mean for your business? Before you can answer this, you need to objectively understand how your new clients would rate their experience of your services to date and how this compares to the satisfaction levels of your longer-term clients.

As you contemplate this, we hope the following insights drawn from our 20+ years of experience helping advisers understand and interpret their own CATScan survey results might provide a little more context.

- The first impression

When a client first comes onboard, what happens in your firm? What’s the client’s first impression? If they feel ‘good’, ‘confident’ or better still ‘delighted’ by their choice, then you’re on the right track. But if they don’t feel this way or, perhaps worse, you don’t actually know, it’s time to get proactive.

A few tips from some advisers we’ve recently worked with about how they create their own distinctive “vibe”:

- Actively seek client’s feedback on what they liked and didn’t like about their onboarding experience and, ask for their suggestions on how your process could possibly be improved. Remember, this is all about the client’s experience, not the adviser or his/ her practice.

- Does your ‘welcome to our practice’ pack make them feel special? Perhaps include a handwritten note from the person who will be servicing the client, introducing themselves and explaining how they can work together to ensure the ‘best’ experience. You could also include a lifestyle questionnaire asking how your client likes to celebrate birthdays, favourite food, favourite sports teams, communities they’re a member of, red or white wine, music preferences etc.

- And as the relationship evolves over time, perhaps the most important driver of client satisfaction is communication. It’s frequency, relevance and level of personalisation all play major roles in keeping clients in the loop, aware and, hopefully, appreciative of their adviser’s efforts.

- What’s the client expecting from you?

Except in a few isolated cases, advisers who underperform in “meeting client expectations” are not actually providing poor service to their new clients. Rather, they have usually failed to explicitly set and manage their new clients’ service delivery expectations.

When left to their own devices (and not knowing any better), new clients will expect the world and demand it yesterday. If you do not take a very active role in clearly defining exactly what you will do and by when, you are setting yourself up to fail. No matter how good your work, or how quickly you deliver, it will almost always underwhelm your new client’s set of self-determined and completely unrealistic expectations.

To minimise the chances of this happening to you, ensure you follow up every meaningful client contact in writing. Clients can sometimes forget the full detail of your discussions so every time you commit to do something, confirm the what, who and when in an email.

Also cut yourself (or at the very least your team) some slack. When committing to timeframes, buy yourself a little time. Unless it is an especially time-critical task, add a day or two to the delivery date. By under promising and over delivering you will not just meet, but consistently exceed the well managed expectations of your new clients.

- Remind me – what do you do again?

We have no doubt that, in some shape or form, all advisers explain to new clients all the different ways in which they can add value. However, it is completely understandable that most of your new clients will be singularly focussed on solving their immediate need – they may not be particularly interested in your other services that are not directly applicable to their current situation.

Providing your new clients with a once only FSG that contains a long list of product names, or creating a services tab on your website, may not be the most effective way to get your message across. You will most likely need to continually educate your clients on the depth and breadth of your solution suite. This includes not just solutions you directly deliver, but also any ancillary services you can facilitate through your strategic alliance network. This will ensure that you and your firm remain the “go-to-solution” for whatever changes life throws at any of your clients.

For your consideration.

On a related note: We will be participating in an Advisely CPD webinar: ‘What your clients don’t tell you’ on Thursday 2 May at 12pm AEST. It’s all about giving advisers and managers a data-driven guide to delivering a better client experience. Hope you can find 30 minutes to join us.

* CATScan Client Satisfaction Survey service The CATScan dataset contains feedback from over 60,000 Australian clients, all of whom are using the services of a financial adviser. As such, these findings are unique in the Australian advice marketplace and exclusive to Business Health.